News Feed

News 2021

Publication: "Modelling Systemic Risk Using Neural Network Quantile Regression"

![]()

Publication

Georg Keilbar's and Weining Wang's paper entitled "Modelling Systemic Risk Using Neural Network Quantile Regression" has been accepted for publication in Empirical Economics.

Congratulations!

Quantlets are available on Github.

Publication: "On Cointegration and Cryptocurrency Dynamics"

![]()

Publication

Georg Keilbar's and Yanfen Zhang's paper entitled "On Cointegration and Cryptocurrency Dynamics" has been accepted for publication in Digital Finance.

Congratulations!

Quantlets are available on Github.

SSRN Top Ten's: Tail-Risk Protection: Machine Learning Meets Modern Econometrics

![]()

SSRN Top Ten Lists

Professor Wolfgang K. Härdle's, Speaker of the IRTG 1792 and Bruno Spilak's paper "Tail-Risk Protection: Machine Learning Meets Modern Econometrics", was recently listed on SSRN's Top Ten download lists for:

02.02.2021: Econometrics: Econometric & Statistical Methods - Special Topics eJournal Top Ten.

We featured this research outlet previously as IRTG 1792 DP 2019-020 here.

SSRN Top Ten's: FRM Financial Risk Meter for Emerging Markets

![]()

SSRN Top Ten Lists

Professor Wolfgang K. Härdle's, Speaker of the IRTG 1792, Michael Althof's and Dr. Souhir Ben Amor's paper "FRM Financial Risk Meter for Emerging Markets", was recently listed on SSRN's Top Ten download lists for:

13.03.2021: ERN: Other Econometric Modeling: International Financial Markets - Emerging Markets (Topic) and Econometric Modeling: International Financial Markets - Emerging Markets eJournal

We featured this research outlet previously as IRTG 1792 DP 2019-020 here.

Publication: "Pricing Wind Power Future"

![]()

Publication

Awdesch Melzer's, Brenda Lopez-Cabrera's, and Wolfgang Karl Härdle's paper entitled "Pricing Green Financial Products" has been accepted for publication as a revised version with Journal of the Royal Statistical Society JRSS-SC-Aug-18-0215.R3 entitled "Pricing Wind Power Futures".

Congratulations!

SSRN Top Ten's: Understanding Smart Contracts: Hype or Hope?

![]()

SSRN Top Ten Lists

Professor Wolfgang K. Härdle's, Speaker of the IRTG 1792, Elizaveta Zinovyeva's, and Raphael C.G. Reule's, MD of the IRTG 1792, paper "Understanding Smart Contracts: Hype or Hope?", was recently listed on SSRN's Top Ten download lists for:

26. April 2021:

- Decision-Making in Computational Design & Technology eJournal Top Ten

- DecisionSciRN: Digital Transformation (Sub-Topic) Top Ten

- DecisionSciRN: Technology Adoption & Diffusion (Topic) Top Ten

- ERN: Technology (Topic) Top Ten

- IRPN: Innovation & Cyberlaw & Policy (Topic) Top Ten

- IRPN: Innovation & Information Management (Topic) Top Ten

- Innovation & Management Science eJournal Top Ten.

27. April 2021:

- Decision-Making in Computational Design & Technology eJournal Top Ten

- DecisionSciRN: Digital Transformation (Sub-Topic) Top Ten

- DecisionSciRN: Technology Adoption & Diffusion (Topic) Top Ten

- ERN: Technology (Topic) Top Ten, IRPN: Innovation & Cyberlaw & Policy (Topic) Top Ten

- IRPN: Innovation & Information Management (Topic) Top Ten

- Innovation & Management Science eJournal Top Ten.

09. May 2021:

- IO: Productivity, Innovation & Technology eJournal Top Ten

10. May 2021:

- IO: Productivity, Innovation & Technology eJournal Top Ten

15. May 2021:

- Innovation Law & Policy eJournal Top Ten

16. May 2021:

- Innovation Law & Policy eJournal Top Ten

29. May 2021:

- Innovation Law & Policy eJournal Top Ten

30. May 2021:

- Innovation Law & Policy eJournal Top Ten

12. June 2021:

- Innovation Law & Policy eJournal Top Ten

13. June 2021:

- Innovation Law & Policy eJournal Top Ten

15. June 2021:

- Industrial Organization & Regulation eJournals Top Ten

16. June 2021:

- Industrial Organization & Regulation eJournals Top Ten

20. June 2021:

- IRPN Subject Matter eJournals Top Ten

- Innovation Disciplines eJournals Top Ten

- Innovation Research & Policy Network Top Ten

21. June 2021:

- IRPN Subject Matter eJournals Top Ten

- Innovation Disciplines eJournals Top Ten

- Innovation Research & Policy Network Top Ten

22. June 2021:

- Decision Science Research Network Top Ten

- DecisionSciRN Subject Matter eJournals Top Ten

23. June 2021:

- Decision Science Research Network Top Ten

- DecisionSciRN Subject Matter eJournals Top Ten

Staff: University of Vienna

![]()

Staff

Georg Keilbar, PhD student of the IRTG 1792, accepted an offer for a postdoc position at the Insitute for Statistics and Operations Research at the University of Vienna.

The University of Vienna (German: Universität Wien) is a public university located in Vienna, Austria. It was founded by Duke Rudolph IV in 1365 and is the oldest university in the German-speaking world. With its long and rich history, the University of Vienna has developed into one of the largest universities in Europe, and also one of the most renowned, especially in the Humanities. It is associated with 21 Nobel prize winners and has been the academic home to many scholars of historical as well as of academic importance. Source

Congratulations and good luck!

Publication: Understanding Smart Contracts: Hype or Hope?

![]()

Publication

Professor Wolfgang K. Härdle's, Speaker of the IRTG 1792, Elizaveta Zinovyeva's, and Raphael C.G. Reule's, MD of the IRTG 1792, paper "Understanding Smart Contracts: Hype or Hope?",

Exclusive Book Chapter

to appear in

“FinTech Research and Applications: Challenges and Opportunities”

[Transformations in Banking, Finance and Regulation series]

to be published by

World Scientific Publishing, July/August 2022

Editors

Daisy Chou, RMIT University, School of Economics, Finance and Marketing, Australia

Conall O’Sullivan, University College Dublin, UCD Michael Smurfit Graduate Business School, Ireland

Vassilios G. Papavassiliou, University College Dublin, UCD Michael Smurfit Graduate Business School, Ireland

Event: First Victoria Peak Conference

![]()

Conference

The First Victoria Peak Conference was organized by the Hong Kong University of Science and Technology, IRTG 1792, and Hamburg University.The conference took place on April 26-27, 2021, online. It covered a broad spectrum of topics on blockchain ecosystem, AI methods for financial applications as well as COVID-19 data analysis from both academic and industrial prospectives.

Wolfgang Karl Härdle, speaker of the IRTG 1792 and many IRTG 1792 doctoral students, amongst them Elizaveta Zinovyeva, Francis Liu, Kainat Khowaja and Xinwen Ni gave talks at the conference.

The respective programmes can be found in the following:

Participation: Finanstilsynet, Financial Supervisory Authority (Denmark)

Participation: Finanstilsynet

Wolfgang Karl Härdle, speaker of the IRTG 1792, Cathy YH Chen, Mercator Fellow of the IRTG 1792, IRTG 1792 doctoral students, amongst them Elizaveta Zinovyeva, and Raphael C.G. Reule, MD of the IRTG 1792, visited the Danish Financial Supervisory Authority (Finanstilsynet) at Copenhagen digitally on July 2nd 2021. It is the financial regulatory authority of the Danish government responsible for the regulation of financial markets in Denmark.

During this Horizon 2020 SupTech Event on "AI, Market Risk and Robo Advisory" they gave talks on "Data Science & Digital Society (DS2)", "Financial Risk Meter (FRM)", "Smart Contracts, and the pursuit of an interdisciplinary technical cure-all", and hosted a coding session.

Event: Big Data and Machine Learning in Finance Conference

![]()

Event: Big Data and Machine Learning in Finance Conference

The conference “Big Data and Machine Learning in Finance“ was organized by the IRTG 1792, the British Retail Consortium, COST, FinTech and the Politecnico di Milano. The conference took place on 10.06.2021- 11.06.2021 via Zoom. The guests were several academicians with diverse backgrounds as well as representatives of the financial industry. The invited speakers were Tomaso Aste (UCL), Emanuele Borgonovo (Università Bocconi), Tucker Balch (JP Morgan AI research), Juri Marcucci (Bank of Italy) and Georgios Sermpinis (Adam Smith Business School, University of Glasgow).

Professor Wolfgang Karl Härdle from the IRTG 1792 was part of the scientific committee.

More informations can be found on the following website:

https://www.mate.polimi.it/fintech/

Participation: Blockchain SupTech Workshop

Participation: Blockchain SupTech Workshop

The “Blockchain SupTech Workshop“ took place on the 17.06.2021 and was organized by the Deutsche Bundesbank. The topics were about blockchains, cryptocurrencies and smart contracts.

Wolfgang Karl Härdle, speaker of the IRTG 1792 and many IRTG 1792 doctoral students gave talks during this workshop.

This workshop was done online via Webex.

More informations about the programm of the workshop can be found on the following website:

Event: EU Fin-Tech Horizon 2020 Final workshop

![]()

Event: EU Fin-Tech Horizon 2020 Final workshop

The final workshop of the “EU Fin-Tech Horizon 2020“ took place on the 18.06.2021 via Zoom and was the final event of a series of many workshops and events.

The topic was the risk management of financial technologies.

Wolfgang Karl Härdle, speaker of the IRTG 1792 opened the event and also gave a talk.

More informations about “EU Fin-Tech Horizon 2020“ and the programm of this event can be found on the following document:

20210530 FINTECH FINAL W UBER Flyer.pdf

Participation: EDT Conference 2021

![]()

Participation: EDT COnference 2021

The conference “Economics of Digital Transformation 2021“ was organized by the University of Rijeka, Faculty of Economics and Business onsite in Rijeka, Opatija and online within the virtual platform from the June 23rd – 25th.

Wolfgang Karl Härdle, speaker of the IRTG 1792, participated as Program Committee and gave a talk on "Understanding Smart COntracts: Hype or Hope?"

More informations can be found on the following website:

https://www.edt-conference.com/index.php

Participation: ITISE 2021 International Conference on Time Series and Forecasting

![]()

Participation: ITISE 2021

On behalf of the 7th International Conference on Time Series and Forecasting (ITISE 2021) Organizer Committee, we would like to thank Souhir Ben Amor, AvH Postdoc, and Wolfgang Karl Härdle, speaker of the IRTG 1792, active participation during this edition of ITISE, which was held from 19th-21th July, 2021 in Gran Canaria (Spain).

Author(s): Souhir Ben Amor and Wolfgang Karl Härdle

Title: An Adaptative Hybrid system based Neurofuzzy model for Energy Price Forecasting

More informations can be found on the following website:

Dissertation: Georg Keilbar completes PhD

20.08.2021. Georg Keilbar defended his PhD dissertation on "Essays on Modern Econometrics and Machine Learning".

Congratulations!

SSRN Top Ten's: Rodeo or Ascot: Which Hat to Wear at the Crypto Race?

![]()

SSRN Top Ten Lists

Professor Wolfgang K. Härdle's, Speaker of the IRTG 1792 and Konstantin Häusler's paper "Rodeo or Ascot: Which Hat to Wear at the Crypto Race?", was recently listed on SSRN's Top Ten download lists for:

24.08.2021:

- ERN: Other Econometric Modeling: International Financial Markets - Volatility & Financial Crises (Topic) Top Ten

- Econometric Modeling: International Financial Markets - Volatility & Financial Crises eJournal Top Ten

20.09.2021

- ERN: Bayesian Analysis (Topic) Top Ten

- ERN: Foreign Exchange Models (Topic) Top Ten

- ERN: Time-Series Models (Multiple) (Topic) Top Ten

- ERN: Time-Series Models (Single) (Topic) Top Ten

- ERN: Volatility (Topic) Top Ten

- Econometric Modeling: International Financial Markets - Foreign Exchange eJournal Top Ten

- Econometrics: Multiple Equation Models eJournal Top Ten

- Econometrics: Single Equation Models eJournal Top Ten.

We featured this research outlet previously as IRTG 1792 DP 2019-020 here.

Dissertation: Raphael Reule completes PhD

03.09.2021. Raphael Reule defended his PhD dissertation on "Digital and Surrogate Finance".

Participation: 4. Blockchain@HTW Conference

![]()

Participation: 4. Blockchain@HTW Conference

Wolfgang Karl Härdle, speaker of the IRTG 1792, Bingling WANG and Min-Bin LIN, IRTG 1792 PhD students, gave a talk on "NFTs and VizTech".

More informations can be found on the following website:

Participation: 29th Annual Conference on PBFEAM

![]()

Participation: 29th Annual Conference on PBFEAM

Wolfgang Karl Härdle, speaker of the IRTG 1792, gave a talk on "FRM the Financial Risk Meter".

More informations can be found on the following website:

http://centerforpbbefr.rutgers.edu

News 2020

News Pictures 2020

")

Participation: Fudan University

![]()

Participation: Fudan University

09.01.2020. Georg Keilbar, PhD student of the IRTG 1792, was visiting Fudan University in Shanghai, China. He gave a talk on “Testing for Neglected Nonlinearity in the Conditional Quantile using Neural Networks” at the Quantitative Economics and Finance Seminar in the School of Economics.

Gender: Dr. A. Petukhina introduces academic junior staff

![]()

Gender

22.01.2020. Dr. Alla Petukhina, LvB Chair of Statistics almuni, introduces our youngest academic junior staff Alexander Maximilian Petukhin, who was born on the 01.11.2019, to our group.

All the best and only the happiest of moments!!

Participation: “Causal Inference and Machine Learning” Workshop St. Gallen

![]()

Participation: “Causal Inference and Machine Learning” Workshop

23.01.2020. Daniel Jacob, PhD student of the IRTG 1792, was visiting the “Causal Inference and Machine Learning” Workshop in St. Gallen. He gave a talk on “Does Tenure Make You Happy in Your Job? – A Machine Learning Approach”. During the two-day workshop keynotes were held by Uri Shalit (Technion - Israel Institute of Technology) and Stefan Wager (Stanford).

Haindorf Seminar 2020

![]()

In cooperation with Charles University Prague, Haindorf Seminar 2020 took place from January 21 to 25 in Hejnice (CZ). During the seminar, PhD students of the IRTG 1792 and Charles University were given the chance to present their current research projects. Additionally to the talks and discussions, Andrew Vivian (Loughborough University/ UK) gave a short course on „Risk Management and Forecasting in Commodity Markets“ and Michael Ellington gave a short course on „Time-Varying Parameter Estimation in VAR models“. Besides the academic program, participants were given the opportunity to go skiing in the nearby Jizera Mountains and to visit the monastery of Hejnice, a historical pilgrimage destination. We thank all participants for their contributions and look forward to continuing the academic prosperous cooperation with Charles University Prague in the future.

There is more information about the participants as well as the talks on the seminar’s website.

Participation: Haindorf Seminar 2020

![]()

Participation: Haindorf Seminar 2020

28.01.2020. In cooperation with Charles University Prague, Haindorf Seminar 2020 took place from January 21 to 25 in Hejnice (CZ). During the seminar, PhD students of the IRTG 1792 and Charles University were given the chance to present their current research projects.

Additionally to the talks and discussions, Andrew Vivian (Loughborough University/ UK) gave a short course on „Risk Management and Forecasting in Commodity Markets“ and Michael Ellington gave a short course on „Time-Varying Parameter Estimation in VAR models“.

Besides the academic programme, participants were given the opportunity to go skiing in the nearby Jizera Mountains and to visit the monastery of Hejnice, a historical pilgrimage destination.

We thank all participants for their contributions and look forward to continue the academic prosperous cooperation with Charles University Prague in the future.

There is more information about the participants as well as the talks on the seminar’s website.

Participation: SFM I Trip to Frankfurt 2020

Participation: SFM I Trip to Frankfurt 2020

20.01.2020. Traditionally, the Statistics of Financial Market I exam takes place during a conclusive educational trip to Frankfurt. Besides the academic program, the students have the possibility to observe how quantitative research and trading departments work in large well-known financial institutions.

This year, two visits were planned: one in the European Central Bank (ECB) and the other in Deutsche Bank AG (DB).

In the ECB main building, the Statistics Department hosted the participants for two tailored lectures on the crypto-asset phenomenon, its risks and measurement issues. The visit was particularly fruitful as one of the speakers, Urszula Kochanska, will be part of the Blockchain Research Center Workshop 2020 organised by the IRTG 1792 in April.

In DB, Christian Schön welcomed the visitors in the Fixed Income trading floor, introducing them to the daily routine of the bank. During the afternoon, Dr. Marius Ascheberg showed the applicability of quantitative skillsets, while Nico Weinert gave an introduction to the Electronic FX trading. To complete the guided tour, Dr. Nicolas David illustrated the mathematical foundation of exotic interest rates derivatives.

We thank Prof. Dr. Wolfgang K. Härdle and the PhD candidate Junjie Hu for having offered this nice opportunity to the students and we are looking forward to the start of Statistics of Financial Market II.

Staff: Natalie Packham appointed Associate Editor for Digital Finance

Participation: Natalie Packham appointed

Associate Editor for Digital Finance

05.02.2020. Natalie Packham, Professor of Mathematics and Statistics at Berlin School of Economics and Law and Associated Researcher at the IRTG1792, and Uwe Wystup, Founder and Managing Direction of MathFinance AG, were appointed Associate Editors of the journal "Digital Finance - Smart Data Analytics, Investment Innovation, and Financial Technology”. They are also Guest Editors of a Special Issue of Digital Finance on Artificial Intelligence, Machine Learning and Platform Innovation in Quantitative Finance to be published in connection with the upcoming MathFinance conference later this year. Welcome on board!

Gender: Marie-Skłodowska-Curie Individual Fellowship

Participation: Marie-Skłodowska-Curie Individual Fellowship

Dr. Rui REN together with Prof. Dr. Weining WANG, applied to the EU Framework Programme for Research and Innovation entitled "Horizon 2020".

They received the Marie-Skłodowska-Curie Individual Fellowship with a amount of 174 806.40 EUR. The type of action is Standard European Fellowship.

The project title is "Quantitative Financial Risk Network Analysis with Sentiment and Herd Behaviour Measures", which is expected to be of 24 months starting within 12 months after the signature of Grant Agreement.

Dr. Rui REN will conduct joint research with Prof. Dr. Weining WANG on tail event driven sentiment network, quantifying investor sentiment, calibrating the option pricing model and detecting herd behaviour in the financial market. It potentially contributes to inclusive, innovative and reflective societies by supporting financial decision-making processes and managing risks for investors and institutions.

Participation: Finanstilsynet, Financial Supervisory Authority (Denmark)

Participation: Finanstilsynet

06.-07.02.2020. Wolfgang Karl Härdle, speaker of the IRTG 1792, Cathy YH Chen, Mercator Fellow of the IRTG 1792, and Raphael C.G. Reule, MD of the IRTG 1792, visited the Danish Financial Supervisory Authority (Finanstilsynet) at Copenhagen, which is the financial regulatory authority of the Danish government responsible for the regulation of financial markets in Denmark.

During this Horizon 2020 SupTech Event on "AI, Market Risk and Robo Advisory" they gave talks on "Data Science & Digital Society (DS2)", "Financial Risk Meter (FRM)", "Smart Contracts, and the pursuit of an interdisciplinary technical cure-all", and hosted a coding session.

Dissertation: N. Wesselhöfft completes PhD

![]()

Dissertation: Niels Wesselhöfft completes PhD

14.02.2020. Niels Wesselhöfft defended his PhD dissertation on "Self Similarity".

Congratulations!

Publication: "Adaptive weights clustering of research papers"

![]()

Publication

20.02.2020. Larisa Adamyan, Kirill Efimov, Cathy Y. Chen and Prof. Wolfgang Härdle's paper entitled "Adaptive weights clustering of research papers" has been accepted for publication in Digital Finance.

The abstract of the paper is as follows:

The JEL classification system is a standard way of assigning key topics to economic articles to make them more easily retrievable in the bulk of nowadays massive literature. Usually the JEL (Journal of Economic Literature) is picked by the author(s) bearing the risk of suboptimal assignment. Using the database of the Collaborative Research Center from Humboldt-Universität zu Berlin we employ a new adaptive clustering technique to identify interpretable JEL (sub)clusters. The proposed Adaptive Weights Clustering (AWC) is available on http://www.quantlet.de/ and is based on the idea of locally weighting each point (document, abstract) in terms of cluster membership. Comparison with 𝑘-means or CLUTO reveals excellent performance of AWC.

Congratulations!

Participation: Bundesbank Horizon 2020 SupTech Event

Participation: Bundesbank Horizon 2020 SupTech Event

10.-11.02.2020. Wolfgang Karl Härdle, speaker of the IRTG 1792, Stefan Lessmann, Principal Investigator of the IRTG 1792, and Rui REN, Postdoc of Fintech Horizon 2020 Project, attended a workshop named “AI, Market Risk and Robo Advisory” at the Deutsche Bundesbank at Frankfurt, which is co-hosted by the Fintech Horizon 2020 Project and the Deutsche Bundesbank.

During this Horizon 2020 SupTech Event, they gave talks on “Financial Risk Meter (FRM)” , “eXplainable AI (XAI) in Regulated Financial Services”, "Interpretable Machine Learning", and “Deep Learning Glossary in Layman Language”, “Network analysis” and “AI Use Cases”.

Publication: "Pricing Cryptocurrency Options"

![]()

Publication

09.03.2020. Ai Jun Hou's, Weining Wang's, Cathy YH Chen's, and Prof. Wolfgang Härdle's paper entitled "Pricing Cryptocurrency Options" has been accepted for publication in Journal of Financial Econometrics.

Congratulations!

Participation: Charles University, Prague

![]()

Participation

11.03.2020. Wolfgang Karl Härdle, speaker of the IRTG 1792, gave a talk on "SONIC: Social Network with Influencers and Communities" at the Charles University, Prague.

The abstract of his talk is given below:

Abstract

The integration of social media characteristics into an econometric framework requires modeling a high dimensional dynamic network with dimensions of parameter Θ typically much larger than the number of observations. To cope with this problem, we introduce a new structural mode SONIC which assumes that (1) a few influencers drive the network dynamics; (2) the community structure of the network is characterized as the homogeneity of response to the specific infuencer, implying their underlying similarity. An estimation procedure is proposed based on a greedy algorithm and LASSO regularization. Through theoretical study and simulations, we show that the matrix parameter can be estimated even when the observed time interval is smaller than the size of the network . Using a novel dataset retrieved from a leading social media platform StockTwits and quantifying their opinions via StockTwits and quantifying their opinions via natural natural language processing, we model the opinions network language processing, we model the opinions network dynamics among a select group of users and further among a select group of users and further detect the latent communities. With a sparsity With a sparsity regularization, we can identify important nodes in the regularization, we can identify important nodes in the network.

SitRep: COVID-19

![]()

Situation Report

13.03.2020. With the Coronavirus situation changing every day, we thought you may appreciate an update from us on how we aim to provide you with uninterrupted research over the coming days and weeks.

As it stands, all of the team here at the IRTG 1792 are fighting fit and healthy and it’s business as usual.

We are closely monitoring developments though, and we are taking extra measures to ensure we stay as healthy as possible and continue to fulfill our duties.

")

Enclosed you find the guidelines of the HU President regarding the immediate measures to prevent the spread of the coronavirus SARS-CoV-2, which were introduced on March 11th 2020. We ask you to observe and comply with the implemented measures and the information given below. Please forward the e-mail/information immediately to the staff in your departments.

Participation: Rheinische Friedrich-Wilhelms-Universität Bonn (University of Bonn)

![]()

Participation

26.05.2020. Rui REN, Anna Shchekina, Vanessa Guarino, and Michael Althof gave a talk on "FRM financialriskmeter for Cryptos", as well did Wolfgang K. Härdle present "Dei ex machinis, the attractiveness of p-hacking".

Publication: "TERES: Tail Event Risk Expectile based Shortfall"

![]()

Publication

12.06.2020. Philipp Gschöpf's, Andrija Mihoci's, and Wolfgang Härdle's paper entitled "TERES: Tail Event Risk Expectile based Shortfall" has been accepted for publication in Quantitative Finance.

Congratulations!

Event: IRTG 1792 Summer Camp 2020

![]()

Event

The annual IRTG 1792 Summer Camp took place at Buckow (Märkische Schweiz) from the 14.07.2020 - 17.07.2020.

Many thanks to all participants and staff, who worked as a team and made this event another successful one for the IRTG 1792. Special thanks to our industrial partners that have joined us, some of who need to remain unnamed, especially from Bitwala and dyos.

We are very glad to have found such a inspiring sanctuary, the Strandhotel Vierjahreszeiten Buckow, with such incredible positive and proactive staff!

")

SSRN Top Ten's: Rise of the Machines? Intraday High-Frequency Trading Patterns of Cryptocurrencies.

![]()

SSRN Top Ten Lists

Professor Wolfgang K. Härdle's, Speaker of the IRTG 1792, Dr. Alla Petukhina's, and Raphael C.G. Reule's, MD of the IRTG 1792, paper "Rise of the Machines? Intraday High-Frequency Trading Patterns of Cryptocurrencies", was recently listed on SSRN's Top Ten download lists for:

31.07.2020: Other Information Systems & eBusiness eJournal Top Ten.

01.08.2020: PSN: Exchange Rates & Currency (International) (Topic) Top Ten.

03.08.2020: International Political Economy: Monetary Relations eJournal Top Ten.

09.08.2020: Capital Markets: Market Microstructure eJournal Top Ten.

We featured this research outlet previously as IRTG 1792 DP 2019-020 here.

News 2019

SSRN Top Ten: Deep Learning-Based Cryptocurrency Sentiment Construction

![]()

SSRN Top Ten List

Professor Cathy YH Chen's, Mercator Fellow of the IRTG 1792, and Dr. Sergey Nasekin's, Alumni of the IRTG 1792, paper "Deep Learning-Based Cryptocurrency Sentiment Construction", was recently listed on SSRN's Top Ten download list for: IRPN: Innovation & Finance (Topic).

The respective website (20.01.2019), with the linked paper and further information, can be reached here.

We featured this research outlet previously as IRTG 1792 DP 2018-066 here.

Participation: WiWi Winterfest 2019

![]()

Participation

17.01.2019: The Chair of Statistics and the IRTG 1792 sponsored culinary activities during this year's Winterfest organized by the School of Business and Economics (WiWi).

")

Participation: IRTG visits CiS systems s.r.o.

![]()

Participation

Researchers and guests of the IRTG 1792 visited the CiS systems s.r.o. We want to thank their staff for taking their time and showing us one of their production locations in the Czech Republic and are looking forward to future activities.

Event: 18. Haindorf Seminar

![]()

Event: 18 Haindorf Seminar

In a long tradition of seminars, the 18. Haindorf seminar, hosted by the IRTG 1792, took place from January 22 until January 26, 2019. In the former Franciscan Monastery in the village of Hejnice (Haindorf) our researchers and guests convened to share and discuss their ongoing research and present their research findings.

Besides the insightful sessions there was enough time for social activity. Participants used the offers of the region such as skiing, hiking and joyful gatherings in the evenings to get to know each other and create a very collegial and friendly atmosphere. The former monastery provided not only adequate rooms for the sessions, the guests and evening activities but also czech food and a guided tour to the associated church and its crypts.

We want to express our sincere thanks to CiS systems s.r.o. for showing us one of their production locations in the Czech Republic.

We look back at a successful Haindorf seminar and look forward to come back to this beautiful place next year again.

There is more information about the participants as well as the talks on the seminar’s website.

Dissertation: L. Adamyan completes PhD

![]()

Dissertation: Larisa Adamyan completes PhD

19.02.2019. Larisa Adamyan defended her PhD dissertation on "Adaptive Weights Community Detection".

Congratulations!

Participation: ZHAW Zurich University of Applied Sciences

![]()

Participation

21.02.2019. Elizaveta Zinovyeva, PhD student of the IRTG 1792, and Dr. Alla Petukhina, alumni of Prof. Härdle, are currently visiting ZHAW Zurich University of Applied Sciences.

We want to thank Prof. Dr. Jörg Osterrieder for cooperating with us on some very important projects, such as an European Commission HORIZON 2020 FinTech Project, and are looking forward to future activities.

Publication: "Dynamic semi-parametric factor model for functional expectiles"

![]()

Publication

07.03.2019. Dr. Petra Budejova's and Prof. Wolfgang Härdle's paper entitled "Dynamic semi-parametric factor model for functional expectiles" has been accepted for publication in Computational Statistics.

Congratulations!

Admin: LvB Website merged with IRTG 1792 website

![]()

Administrative

01.04.2019. The "Ladislaus von Bortkiewicz Chair of Statistics" website has been merged with the IRTG 1792 website. All previous content from that website is kept accessible.

Furthermore, we invite all colleagues to regularily use the black board on the first floor. Here you can see Cathy YH Chen, Antonio Galvao and Jozef Barunik working with it.

Participation: METIS - gender equality and family-friendliness

![]()

Participation: METIS

04.04.2019. The IRTG 1792 is very happy to be part of the alliance that offers a new resource to the HU Berlin research community: www.metis.hu-berlin.de .

The objective of this platform is to offer assistance with respect to the academic and personal development of the members of the research community by providing support to female scientists, creating more family-friendliness and reducing gender stereotypes in the work environment.

The platform offers information about upcoming events, workshops and publications on gender equality issues. Furthermore, in the SERVICES FOR MEMBERS section provides inspiration for types of projects that can be financed though the platform.

For more information and potential gender equality projects, don’t hesitate to contact Dr. Anne Freese or Raphael C. G. Reule.

Event: MathFinance Conference 2019

![]()

Event: MathFinance Conference 2019

08.04.2019. Professor Wolfgang K. Härdle and Professor Natalie Packham gave talks at the MathFinance Conference 2019: The Quant Conference in Frankfurt, Germany.

MathFinance, founded by Uwe Wystup in 2003, is an independent consulting and software company specializing in risk management of derivatives in all asset classes. Their pricing libraries, consulting in exotic options and structured products, independent studies have been used by a variety of banks, asset managers, and software companies.

MathFinance is a quantitative finance advisory firm, which specializes in the development of state-of-the art models for trading, sales and risk management. They focus strongly on FX options, the volatility surface and structured derivatives, where they have in-house software. Their team of experts has a strong quantitative background and many years of practical experience in front-office environments as quants, structurers and traders.

Their affinity to both the industry and the academia lets them approach and tackle a problem from all possible angles and provides a tailor-made solution grounded on both extensive research and hands-on practice.

They offer in-house and public derivatives trainings and organize the annual MathFinance Conference in Frankfurt since 2000. Their best-seller course that runs from Sydney to Salt Lake City is Foreign Exchange Derivatives.

Publication: "Network quantile autoregression"

![]()

Publication

11.04.2019. Xuening Zhu's, Weining Wang's and Wolfgang Härdle's paper entitled "Network quantile autoregression" was published in the Journal of Econometrics.

https://doi.org/10.1016/j.jeconom.2019.04.034

https://www.sciencedirect.com/science/article/pii/S0304407619300892?via%3Dihub

Congratulations!

Event: Energy Finance Workshop 2019

![]()

Event: Energy Finance Workshop 2019

17.04.2019. Researchers from the Universität Duisburg-Essen, Humboldt-Universität zu Berlin and Universität St. Gallen have met once again to work together and to enjoy some joint sport activities during the Energy Finance Workshop 2019.

Once again his years programme is presenting a very interessting range of research topics, and we are very happy to have some of our students to be able to present at this occasion, especially Awdesch Melzer, who will soon graduate from our institution.

Dissertation: A. Melzer completes PhD

![]()

Dissertation

18.04.2019. Awdesch Melzer defended his PhD dissertation on "Dynamics of day-ahead electricity prices".

Congratulations!

SSRN Top Ten's: Understanding Cryptocurrencies

![]()

SSRN Top Ten Lists

Professor Wolfgang K. Härdle's, Speaker of the IRTG 1792, Professor Campbell R. Harvey's, and Raphael C.G. Reule's, Director of the IRTG 1792, paper "Understanding Cryptocurrencies", was recently listed on:

07.05.2019. SSRN's Top Ten download lists for: Derivatives eJournal Top Ten, ERN: Futures (Topic) Top Ten, ERN: Stock Market Risk (Topic) Top Ten and Econometric Modeling: Derivatives eJournal Top Ten.

08.05.2019. The reasearch was also listed in the Top Ten lists for Banking & Insurance eJournal Top Ten and Econometric Modeling: Capital Markets - Risk eJournal Top Ten.

09.05.2019. The paper was furthermore listed in the Top Ten for Capital Markets: Market Microstructure eJournal Top Ten.

11.05.2019. Top Ten for ERN: Asset Pricing Models (Topic) Top Ten.

12.05.2019. Top Ten list for: Capital Markets: Asset Pricing & Valuation eJournal Top Ten and Capital Markets: Asset Pricing & Valuation eJournals Top Ten.

19.05.2019. Top Ten list for: Econometric Modeling: Capital Markets - Asset Pricing eJournal Top Ten.

25.06.2019. Top Ten list for: Econometric Modeling: Financial Markets - Capital Markets eJournals Top Ten.

01.07.2019. Top Ten list for: Capital Markets: Asset Pricing & Valuation eJournal Top Ten, Capital Markets: Asset Pricing & Valuation eJournals Top Ten, Econometric Modeling: Financial Markets eJournals Top Ten and Mutual Funds, Hedge Funds, & Investment Industry eJournal Top Ten.

03.01.2022 Top Ten download list for: ERN: Futures (Topic) Top Ten.

04.01.2022 Top Ten download list for: ERN: Futures (Topic) Top Ten.

We featured this research outlet previously as IRTG 1792 DP 2018-044 here.

Dissertation: Y. Qian completes PhD

![]()

Dissertation

06.05.2019. Ya Qian defended her PhD dissertation on "Industry Interdependency Dynamics in a Network Context".

Congratulations!

Publication: "Model-driven statistical arbitrage on LETF option markets "

![]()

Publication

23.05.2019. Sergey Nasekin's and Wolfgang Härdle's paper entitled "Model-driven statistical arbitrage on LETF option markets" is now on Taylor & Francis Online.

https://doi.org/10.1080/14697688.2019.1605186

Participation: Advances in Econometrics, Volume 42, The Econometrics of Networks

![]()

Participation

29.05.2019. Xinwen Ni, PhD student of the IRTG 1792, visited the "Advances in Econometrics, Volume 42, The Econometrics of Networks" conference and presented "Textual Sentiment and Sector specific reaction". The conference was in Paltinis, Romania from May 16 to 17, 2019.

Participation: Economic Applications of Quantile Regression 2.0

![]()

Participation

08.06.2019. Georg Keilbar, PhD student of the IRTG 1792, visited the conference “Economic Applications of Quantile Regression 2.0” and presented “Modelling Systemic Risk using Neural Network Quantile Regression”. The conference was in Lisbon, Portugal from June 7 to June 8, 2019.

Gender: HUB & XMU Girls on the Muddy Angel Run

![]()

Gender

16.06.2019. Ioana Ceausu, Elizaveta Zinovyeva, Lili Matic, Elena Ivanova and Bingling Wang, IRTG 1792 PhD students, as well as Yanfen Zhang, XMU PhD student, teamed up and joined MUDDY ANGEL RUN - EUROPE’S 5K WOMEN-ONLY MUD RUN!, which was funded through IRTG 1792 researchers.

The “Muddy Angel Run” is Europe’s 5 kilometer Mud Run for women of all fitness levels who want to do good while having fun.

Whether running, jogging or walking. Whether young or old, whether a small or large donation: connect with other angels from your friends, colleagues, and family. Get your sisters, your mother, daughters, neighbors, colleagues in your team to have fun and do good!

Worldwide over one million women have participated in Mud Runs against breast cancer. With your participation in the Muddy Angel Run you support this movement and become part of a unique community.

")

News 2018

Seminar: Haindorf 2018

30.01.2018. 17th Haindorf seminar hosted by the IRTG 1792 took place from January 23 until January 27, 2018.

In a long tradition of seminars, the 17th Haindorf seminar hosted by the IRTG 1792 took place from January 23 until January 27, 2018. In the former Franciscan Monastery in the village of Hejnice (Haindorf) our researchers and guests convened to share and discuss their ongoing research and present their research findings.

Besides the insightful sessions there was enough time for social activity. Participants used the offers of the region such as skiing, hiking and joyful gatherings in the evenings to get to know each other and create a very collegial and friendly atmosphere. The former monastery provided not only adequate rooms for the sessions, the guests and evening activ-ities but also Czech food and a guided tour to the associated church and its crypts.

We want to express our sincere thanks to the CEO of CiS systems s.r.o., Mr. Peter M. Wöllner, for taking his time and showing us one of his production locations under his supervision in the Czech Republic.

We look back at a successful Haindorf seminar and look forward to come back to this beautiful place next year again.

There is more information about the participants as well as the talks on the seminar’s website.

Publication: Dr. Xiu Xu's paper "lCARE - localizing Conditional AutoRegressive Expectiles" has been accepted for publication in Journal of Empirical Finance

10.01.2018. We have been informed that the paper "lCARE - localizing Conditional AutoRegressive Expectiles" by the IRTG alumni Dr. Xiu Xu has been accepted for publication in Journal of Empirical Finance.

We now look forward to seeing their article appear in a future issue of JE.

The article will be based on the SFB 649 Discussion Paper 2015-52.

Our most recent discussion papers are available in our research results section.

Publication: Prof. Härdle and Prof. Chen publish in Journal of Econometrics

08.01.2018. We have been informed that the paper "Tail event driven networks of SIFIs" by the IRTG professors Prof. Wolfgang Karl Härdle and Prof. Cathy Yi-Hsuan Chen and Prof. Yarema Okhrin (University of Augsburg) submitted to The Journal of Econometrics will be accepted.

We now look forward to seeing their article appear in a future issue of JE.

The article will be based on the SFB 649 Discussion Paper 2017-004.

Our most recent discussion papers are available in our research results section.

Dissertation: T. Benschop completes PhD

Dissertation: T. Benschop completes PhD

24.11.2017. Thijs Benschop, IRTG PhD student, defended his PhD dissertation on "Modeling the CO2 Markets". Congratulations!

Dissertation: X. Xu completes PhD

Dissertation: X. Xu completes PhD

13.11.2017. Xiu Xu, IRTG PhD student, defended her PhD dissertation on "Hedging with Spectral Risk Measure" with Magna Cum Laude. Congratulations!

Dissertation: S. Chen completes PhD

Dissertation: S. Chen completes PhD

17.11.2017. Shi Chen, IRTG PhD student, defended her PhD dissertation on "Risk management" with Summa Cum Laude. Congratulations!

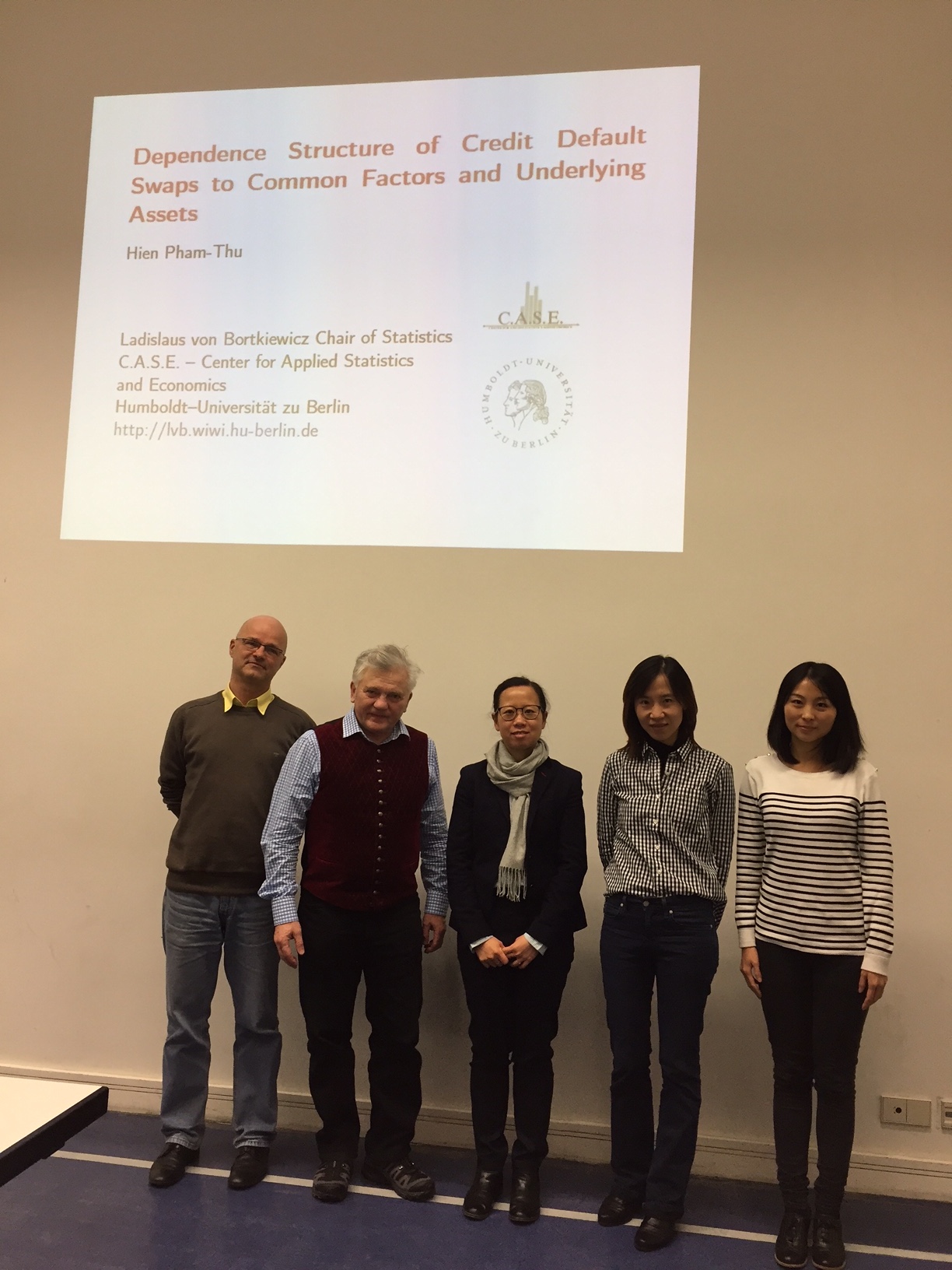

Dissertation: H. P. Thu completes PhD

Dissertation: H. P. Thu completes PhD

31.01.2018. Hien Pham Thu defended her PhD dissertation on "Dependence Structure of Credit Default Swaps to Common Factors and Underlying Assets". Congratulations!

LMU Munich - Postdoctoral position DFG project

![]()

LMU Munich - Postdoctoral position DFG project

The Working group Biostatistics at the LMU Munich is offering a Postdoctoral position within the framework of the DFG project "Statistical Modeling using mouse movements to model measurement errors and improve data quality in web surveys".

Please take a look at the projects website and the job offer, if you are interested.

Dissertation: A. Zharova completes PhD

Dissertation: A. Zharova completes PhD

08.02.2018. Alona V. Zharova, PhD student, defended her PhD dissertation on "Measures of University Research Output" with Summa Cum Laude. Congratulations and all the best for her future career in academia - we certainly have to expect more to come from this extraordinary young researcher!

Open SHK Positions

![]()

IRTG 1792 - Open SHK Positions

The coordination office is looking for energetic, professional and team work oriented members to join us. This opening comes with the opportunity to grow with our doctoral programme using your current skills, as well as applying skills you will pick up on the job.

Hard facts:

- Employment place: IRTG 1792, Coordination Office, School of Business and Economics

- Employment period: 24 months

- Work time: 41 hours per month

- Application periode: 19.02.2018 - 12.03.2018

Duties will include:

- Work in the coordination office of the IRTG 1792

- Literature research and procurement

- Maintenance of databases

- Maintenance of websites

Skills and Experiences Preferred

- Study of a subject relevant to the area of responsibility

- Knowledge of common MS-Office programs

- Independent and reliable work attitude

- Experience in team and project work

- Mandatory knowledge: SQL, JavaScript and PHP

- Advantageous knowledge (not a requirement): Linux and R

Great staff benefits

- Work with a motivated team in an international academic research environment

- Growth opportunity in a growing international research organisation

- Vibrant international cultural exchange

- Learning about new research techniques and learning new skills through academic contacts

- The opportunity to network with international research professionals through off site events or training courses.

Please send your application (including a motivation letter stating your study interests and plans, an curriculum vitae and information on previous studies (i.e. transcripts and certificates in regards to the position) by 12.03.2018, quoting reference number 70/06/18 and the subject IRTG 1792 STR SHK to the Humboldt-Universität zu Berlin, School of Business and Economics, IRTG 1792 "High Dimensional Nonstationary Time Series", Unter den Linden 6, 10099 Berlin or preferably via eMail to irtg1792.wiwi@hu-berlin.de.

The Humboldt-Universität zu Berlin is seeking to increase the proportion of women in academia, and specifically encourages qualified female students to apply. Severely disabled applicants with equivalent qualifications will be given preferential consideration. People with an immigration background are specifically encouraged to apply. Since we will not return your documents, please submit copies in the application only.

We are looking forward to your application.

Click to enlarge.

News 2017

Our Team: New IRTG Managing Director

01.01.2017 Alona Zharova to be new IRTG Managing Director starting from 1.1.2017. Welcome to the

IRTG!

Research visit: C. Huang in Cambridge

05.01.2017. Chen Huang was invited to visit Cambridge University 2017.3 - 2017.6. She will work with Oliver Linton, IRTG Advisory Board member, on high

frequency data.

Publication: Paper accepted to JAM

13.01.2017. The paper "Tail Event Driven Asset Allocation: evidence from equity and mutual funds' markets" by W.K. Härdle, S. Nasekin and A. Petukhina was accepted to the Journal of Asset Management"

Dissertation: S. Nasekin completes PhD

20.01.2017. Sergey Nasekin, IRTG PhD student, defended his PhD dissertation on "Dynamic Dimension Reduction for Financial Applications" with Summa Cum Laude. Congratulations!

Conference: Haindorf Seminar 2017

24.01.2017. This year, the Haindorf conference has attracted speakers and short course lecturers from Charles University in Prague (CZ), National Taiwan University (TW), National Taipei University (TW), Hanyang University (KR) and Massachusetts Institute of Technology (US) who presented their newest research findings. The snowy hills of Haindorf created a warm and productive athmosphere indeed! Thanks to Lenka Zbonakova, IRTG PhD student, for the great organization!

Our team: Position for S. Trimborn

03.02.2017.Simon Trimborn, IRTG PhD student, received an offer by National University Singapure (SG) to continue his PhD studies in the Department of Statistics and Applied Probability. Congratulations!

Dissertation: F. Schulz completes PhD

06.02.2017. Franziska Schulz, IRTG PhD student, ended her doctoral study on "Probabilistic Models in Energy Finance" with a brilliant defense with Summa Cum Laude. Congratulations!

Dissertation: L. Fang completes PhD

07.02.2017. Lei Fang, the former IRTG Manager, successfully finished her doctoral studies on "Mortality Models and Longevity Risk". Congratulations!

Spring School: K. Papagiannouli in Malente

20.02.2017. The IRTG doctoral student Katerina Papagiannouli presented her work at the Spring School of Research unit 1735: Structural inference in Statistics in Malente, from 20.02.2017 until 25.02.2017. The topic of her talk was Estimation of Cointegrated volatility in the presence of Jumps.

Seminar: L. Zbonakova at Charles University Prague

14.06.2017. Lenka Zbonakova, an IRTG students, presented her work at a research seminar on 14.6.2017 at the Institute of Economic Studies, Faculty of Social Sciences, Charles University in Prague. The topic of her talk was "Penalized Adaptive Method", which is an IRTG joint work with Prof. Wolfgang Härdle and the IRTG student Xinjue Li.

Conference: New York University

21.06.2017. Prof. Wolfgang Härdle, the IRTG coordinator and spokesperson, organised a session at the SoFiE conference at New York University on „Cryptos, mining and sentiment surprises".

Seminar: Prof. Härdle at the European Central Bank

19.06.2017. Prof. Wolfgang Härdle, the IRTG coordinator and spokesperson, held a seminar at the European Central Bank on „Tail Event Driven Networks of SIFIs".

Conference: Charles University Prague

16.06.2017. Prof. Wolfgang Härdle, the IRTG coordinator and spokesperson, presented his talk on "Textual Sentiment and Sector-specific Reactions" at Charles University Prague.

Workshop: Prof. Härdle at TU Dresden

14.06.2017. Prof. Wolfgang Härdle, the IRTG coordinator and spokesperson, attended the workshop „Big Data in Logistics" at TU Dresden and held his presentation on „Dynamic Topic Modelling for Crypto Currency Fora".

Workshop: FinTech at UCL

19.06.2017. Hermann Elendner, IRTG associated researcher, presented his talk about "Cryptocurrency Evolution and the Resiliency of Blockchain Markets" at the workshop "Blockchain and the Constitution of a New Financial Order: Legal and Political Challenges" that was held at University College London today on June 06th.

From the website: "The workshop deals with emergent economic, political and legal phenomena in the field of FinTech. It pursues two distinct goals. First, it intends to generate awareness and facilitate a better understanding of the actors, phenomena and dynamics of the new financial order. Second, it explores the political and legal implications of financial and technological innovation based on blockchain technology."

Dissertation: M. Lu completes PhD

16.06.2017. Mengjou Lu, IRTG PhD student, successfully defended his PhD dissertation. Congratulations!

Book Release: Applied Quantitative Finance

09.06.2017. The editors Wolfgang Härdle, Cathy Yi-Hsuan Chen and Ludger Overbeck published their new book "Applied Quantitative Finance" with content by the IRTG 1792 students Shi Chen and Lenka Zboňáková and the IRTG 1792 participating researcher Prof. Weining Wang.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

.jpeg){kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

.jpeg){kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Our team: Job offer for T. Benschop

01.06.2017. PhD graduate Thijs Benschop will continue his career at the Bureau for Economic Policy Analysis (CPB) in Haag, Netherlands. Congratulations, Thijs!

Workshop: Energy Finance

05.05.2017. For the fifth time the annual Energy Finance Workshop took place in the beautiful village of Stolberg in the Harz from April 19 - 21. Fifteen participants from the Ladislaus von Bortkiewicz Chair of Statistics, Humboldt-Universität zu Berlin and the Chair for Energy Trading and Finance, University of Duisburg-Essen presented their on-going research in a friendly and inspiring atmosphere.

Energy markets are developing rapidly, with new marketplaces emerging globally for electricity, weather and emissions. The Energy Finance workshop Stolberg 2017 focused on recent trends in modelling and management of risk in energy markets. The topics included, but were not limited to wind energy, emission trading, commodity markets and applied advanced statistical and forecasting methods.

Our Researchers appointed INDI Fellows

19.04.2017. Wolfgang Härdle, Vladimir Spokoiny and Yongmiao Hong became Fellows of the Institute for Nonlinear Dynamical Inference (INDI) at RUDN University in Moscow. Among other INDI Fellows are Angus Deaton (2015 Nobel Laureate in Economics), Robert F. Engle (2003 Nobel Laureate in Economics), Lars Peter Hansen (2013 Nobel Laureate in Economics), James J. Heckman (2000 Nobel Laureate in Economic), Daniel McFadden (2000 Nobel Laureate in Economics) and Christopher A. Sims (2011 Nobel Laureate in Economics).

News 2016

Research visit: Singapore Management University

10.12.2016. Ya Qian, IRTG PhD student, was invited to Singapore Management University (SMU) for a research visit from May to July 2017

Our team: Job offer for S. Nasekin

01.12.2016. Sergey Nasekin, IRTG PhD student, received an offer from Lancaster University (UK) and decided to continue his academic career at the Lancaster University. Congratulations!

Workshop: Seminar of the HypoVereinsbank-UniCredit Group

21.10.2016 – 22.10.2016. The IRTG doctoral student Awdesch Melzer attended the PhD Seminar Seminar of the HypoVereinsbank-UniCredit Group-Stiftungsfonds in memoriam Giovanna Crivelli in Leipzig, Germany. Awdesch Melzer presented his paper “Pricing Green Financial Products”.

Workshop: IRTG Workshop Rumble in the Jungle

13.10.2016 – 15.10.2016. The IRTG organized its annual workshop "Rumble in the Jungle" for its doctoral students, invited guests and its participating faculty in Grünheide, Germany. The students were provided with an opportunity to talk about their current research, Awdesch Melzer, for instance, presented his paper “Pricing Green Financial Products”.

Internship: N. Wesselhöfft at Deutsche Bank

31.08.2016. PhD student Niels Wesselhöfft has just finished his six-month internship in the Asset and Wealth Management Department of Deutsche Bank. Congratulations!

Publication: Paper accepted to JASA

20.07.2016. The paper “Forecasting Generalized Quantiles of Electricity Demand: A Functional Data Approach” by Brenda López Cabrera and Franziska Schulz was accepted to the Journal of the American Statistical Association.

Research visit: Princeton University

11.07.2016. PhD student Franziska Schulz will leave today for a research stay at Princeton University, USA.

Workshop: BTU Cottbus hosting IRTG students

11.07.2016. Andrija Mihoci, former IRTG Postdoctoral Researcher, has organized a workshop in BTU Cottbus-Senftenberg on "Quantitative Methods in Economics" on 10.-11.07.2016 and invited IRTG members to present their research results.

Conference: Paper presented at Energy and Commodity Finance Conference

24.06.2016. Thijs Benschop und Awdesch Melzer, two IRTG students, attended the Energy and Commodity Finance Conference in Paris. Thijs presented his paper on “Modeling and forecasting of realized volatility of CO2 emission futures contracts” and Awdesch presented his paper on “Wind Energy Risk Modelling”.

Workshop: Lenka Zboňáková in Xiamen

19.06.2016. Lenka Zboňáková, IRTG PhD student, visited the “WISE-CASE Workshop on Digital Economy and Decision Analytics” in Xiamen from 18.-19.06.2016 and presented her work on “Time Varying Lasso”.

Conference: Presentation at Commodity Markets Conference, Hannover

04.06.2016. Thijs Benschop attended the Commodity Markets Conference in Hannover, Germany and presented his work on “Volatility Modelling of CO2 Emission Allowance Spot Prices with Regime-Switching GARCH Models”.

Conference: PhD student presents at Dynstoch

02.06.2016. Sebastian Holtz, PhD student, presented his work on ”Parametric covariation from noisy observations: efficiency, equivalence and estimation” at Dynstoch 2016 in Rennes, France.

Research visit: Xiamen University

01.05.2016. Lenka Zboňáková, IRTG PhD student, is currently on a research stay at CASE in Xiamen, China. She will be working on "Time Varying Lasso" from 10.04.2016 until 30.06.2016.

Research visit: Singapore Management University

23.04.2016. PhD student Simon Trimborn was invited for his second research stray at the Singapore Management University, Singapore in August. Congratulations!

Workshop: Participation in Energy Finance Workshop

22.04.2016. The IRTG doctoral students Thijs Benschop, Shi Chen and Awdesch Melzer

attended the Energy Finance Workshop 2016 in Stolberg, Germany. Thijs Benschop presented his paper on “Modeling and forecasting of realized volatility of CO2 emission futures contracts”, Awdesch Melzer presented his project “Wind Energy risk Modelling”.

Conference: Presentation at DAGStat Conference

18.03.2016. PhD student Franziska Schulz presented her paper “Germany Probabilistic Forecasts of Electricity spot prices: A functional data approach” at the DAGStat Conference in Göttingen, Germany.

Thijs Benschop also presented his work on “Modeling and forecasting of realized volatility of CO2 emission futures contracts” at the conference.

Publication: Paper accepted to JE

11.02. 2016. The paper “TENET - Tail Event driven NETwork risk” by Wolfgang Härdle, Weining Wang and Lining Yu was accepted to the Journal of Econometrics.

Conference: Haindorf Seminar 2016

30.01.2016. In this year’s Haindorf seminar, speakers from Cambridge University (UK) and the University of Szczecin (PL) presented their newest research findings. The winter landscape did not only set up a good atmosphere, but also led to some ski rides.

Research visit: University of Pennsylvania

03.01.2016. Sergey Nasekin, IRTG PhD student, was invited to the University of Pennsylvania, USA for a two-month research stay from March to May 2016.

Research visit: Princeton University

15.01.2016. PhD student Sergey Nasekin was invited to visit Princeton University, USA for a two-week research stay from the End of February to the beginning of March.

News 2015

Publication: Paper accepted to JBCB

11.12.2015. The paper “Detection of homologous recombination in closely related strains” by Anastasia S. Kalinina, Alexandra L. Suvorikova, Vladimir G. Spokoiny and Mikhail S. Gelfand was accepted to the Journal of Bioinformatics and Computational Biology.

Conference: Lenka Zboňáková in Vienna

09.12.2015. Lenka Zboňáková, IRTG PhD student, visited the conference on “Risk Management in Very High Dimensions” in Vienna, Austria and presented her work on “Time Varying Lasso”.

Publication: Paper accepted to “Energy Economics”

11.11.2015. The paper “Volatility Linkages between energy and agricultural commodity prices” by Brenda López Cabrera and Franziska Schulz was accepted to Energy Economics.

Workshop: Cambridge hosting IRTG students

08.12.2015. PhD students Alla Petukhina and Chen Huang visited the conference on “New Directions on Quantile Regression” at Trinity College, University of Cambridge and presented their work on “TEDAS with τ-spine optimization” and “Factorizable Sparse Tail Event Curves with Expectiles”.

Workshop: Rumble in the Jungle

06.10.2015. The new generation of students was warmly welcomed at the Rumble in the Jungle Workshop in Berlin. Besides many interesting presentation and promising project proposals, the great location near the Peetzsee set a nice and bright working environment.

Conference: Presentation at CEQURA Conference

02.10.2015. Lei Fang, PhD student, attended the CEQURA Conference and presented her paper on “A Mortality Model for Multi-populations: A Semi Parametric Approach”.

Our team: Job offer for A. Mihoci

01.10.2015. Andrija Mihoci, IRTG Postdoctoral Researcher, became W3 professor in Brandenburgische Technische Universität Cottbus-Senftenberg (DE). Congratulations!

Summer School: Information Retrieval

15.09.2015. Larisa Adamyan, PhD student, completed the Russian Summer School in Information Retrieval 2015 in Saint Petersburg on “Unsupervised Lemmatization using Wiktionary”.

Research visit: National University of Singapore

04.09.2015. Simon Trimborn, IRTG student, was invited by the National University of Singapore for a two-week research stay in December. He will work together with Prof. Ying Chen.

Internship: European Central Bank

31.07.2015. PhD student Thijs Benschop has just successfully finished his five-month internship at the European Central Bank in the Monetary and Financial Statistics (MFS) division of the Directorate General Statistics.

Conference: Participation at BSHS

12.07.2015. Alla Petukhina hold a presentation on “Collective Biographies - the Database BBI - Biographical Background Information” at the British Society for the History of Science (BSHS) 2015 Conference in Swansea, UK.

Dissertation: S. Chao completes PhD

02.06.2015. Shi-Kang Chao finished his PhD dissertation on "Quantile Regression in Risk Calibration" and took a visiting professorship at Purdue University (US). Congratulations!

Workshop: Participation in Cambridge

19.05.2015. The PhD students Xiu Xu and Lining Yu participated in the Workshop on tail event driven risk modeling at Cambridge University, UK with a presentation on “TENET: Tail-Event driven Network Risk”.

Research visit: Invitation from Lancaster University

20.03.2015. IRTG manager and doctoral student Lei Fang was invited to a research stay at Lancaster University in May this year! She will work with Prof. Park Juhyun on a mortality model for multi-populations.

Workshop: Presenting in Russia

17.03.2015. Alexandra Suvorikova, doctoral student, presented her work on “Local Change-Point Detection” at the Workshop “Frontiers of High Dimensional Statistics, Optimization, and Econometrics” in Moscow, Russia.

Workshop: A. Petukhina in Singapore

16.03.2015. Alla Petukhina presented her paper on “Tail Event Driven ASset allocation: evidence from equity and mutual funds’ markets” at the TEDRIS - Tail Event Driven RIsk Structures Workshop in Singapore.

Research visit: Singapore Management University

07.03.2015. Alla Petukhina, doctoral student of the IRTG, starts her research stay at Singapore Management University today.

Internship: Deutsche Bank Research

01.03.2015. We wish our PhD student Niels Wesselhöfft a successful start for his internship at Deutsche Bank Research!

Conference: Haindorf Seminar 2015

31.01.2015. The Haindorf seminar in 2015 started with a short course from Qiwei Yao, London School of Economics (UK) and continued with many more enlightening presentations from speakers form Charles University (CZ), Lancaster University (UK), National Taiwan University (TW) and more.

Workshop: Jour Fixe Winter 2015

21.01.2015. The Winter Jour Fixe this year brought along many participants across economics, statistics and mathematics departments from Humboldt and other universities from Europe, North America and Asia. Prof. Wolfgang Härdle gave a warm welcome to the Jour Fixe participants as well as visiting guests such as Prof. Rohit Deo (NYU Stern), Meng Jou Lu (National Chiao Tong University), Yun Cheng Tsai (National Taiwan University) and Frank Tan (Singapore Management University). This was followed by Lining Yu (IRTG student), giving an introduction to the newly developed CRC Financial Risk Index, also known as financial risk meter.

News 2013

Research visit: Singapore Management University

12.12.2013. Simon Trimborn was invited for a research stay at the Singapore Management University in March.

Workshop: Energy Finance 2013

12.10.2013. Thijs Benschop and Franziska Schulz presented their works on “Volatility Modelling of CO2 Spot Prices Using Markov Switching Models” and “Forecasting Conditional Quantiles of Electricity Demand” at the Energy Finance Workshop in Essen, Germany. Franziska also presented her findings at the Applicable Semiparametrics Conference in Berlin, Germany.

Research visit: Fields Institute in Toronto

28.07.2013. In one week, the PhD student Franziska Schulz will leave to Toronto for a one-month research stay at the Fields Institute in Toronto, Canada.